I’m scared I’ll lose money if I invest. How do I face my fear?

I’ve been looking into investing in ETFs. My big hesitation is fear. I don’t want to lose money. I’ve heard a lot of horror stories, and the news headlines since COVID haven’t been very encouraging, with some kind of recession or economic crisis always around the corner. I keep thinking I should wait until things are more stable, but it’s been some years now, so I guess that’s not going to happen. How do I pull the trigger?

You’re right. Waiting for things to stabilise isn’t a good idea. That’s like waiting for the waves in the ocean to smooth over before you jump in. It’s against the very nature of the economy and markets. You’ve got to jump in. But how?

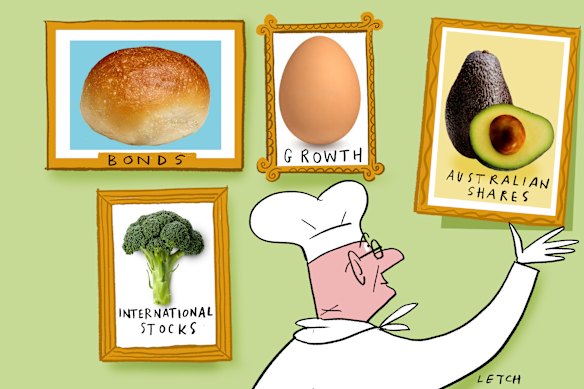

Investing is a bit like having a healthy diet: it isn’t about one specific food, it’s about the balance of what you eat overall.Credit: Simon Letch

Sure, there is an element of courage required. But there are things you can be doing to manage and mitigate risk as well, which will help you feel safer to make the jump.

Here are some questions you can ask yourself that will help you de-risk investing.

What’s your investing time-horizon?

I’d be happy to assume that a significant portion of the horror stories you hear are not about people “losing” money in investments, but about people not being able to hang on through a rough market.

In other words, if they’d kept the money invested and waited a bit (instead of selling the investments in fear) they would have come good in a few months or years.

If you throw everything into investments, and don’t have enough savings – what will you do if you lose your job?

While markets are volatile in the short term, over the long term generally they trend upwards. This means if you zoom in and look at any one- to five-year time period, the market will look quite random. But if you zoom out and look at that same market over decades (10 to 20-plus years), despite all the ups and downs in between, overall the market would have gone up over time.

In short, volatility (and risk) are higher over shorter time periods. So one way to significantly de-risk your investments is to have a long-term time-horizon. Think in decades, not years.

What’s your asset allocation?

Asset allocation is the split of your investments across different asset classes – how much of your portfolio is in growth assets (like shares, property, etc.) versus defensive assets (such as bonds).

There’s research to suggest that asset allocation is one of the most important factors in portfolio design – even more important than the specific investment choice itself.

Good investing is not about betting on the one winning horse that’s going to make you rich. It’s about designing an overall portfolio and strategy that, as a whole, will achieve your long-term financial goals. Another way to think about it is: eating a healthy diet isn’t about one specific food, it’s about the balance of what you eat overall.

Having a good balance of defensive and growth assets helps balance out the risk profile of different asset classes, so you’re not too heavily exposed to the risk of a single asset class.

Loading

What should that balance be? Typically, the younger you are, the more you can afford to have a heavier weighting towards growth (riskier) assets because you have time to ride out any market crashes, whereas the closer you get to retirement you want to start introducing more defensive assets to your portfolio to protect your assets against any significant downturns.

What are your financial buffers?

If not having a long enough time horizon is one big reason why people lose money in investments, the other is not having sufficient financial buffers (and the two are related).

If you want to keep your money invested through the ups and downs of the market, you need to have enough cash on hand to see you through short- and midterm expenses.

If you throw everything into investments and don’t have enough savings, what will you do if you lose your job, get into an accident, or have an unexpected medical emergency? You will probably have to sell your investments to pay for those things, and if you prematurely have to sell your investments, the timing might not be ideal.

Having financial buffers to see you through emergencies reduces the risk you’ll be in a position where you have to sell your investments at a bad time in the market.

You can’t run from risk. It’s everywhere. Choosing not to invest has risks. Keeping money in savings has risks. It’s not really less risky. It’s just a different risk.

The only real path out is to learn to identify, mitigate and manage risk. Then you’re no longer scared of risk. You understand it. You have the strategies and systems in place to manage it with confidence. It’s no longer a threat to run from. In fact, you see that it’s a tool to build wealth, once you know how to use it.

Paridhi Jain is the founder of SkilledSmart, which helps adults learn to manage, save and invest money through financial education courses and classes.

- Advice given in this article is general in nature and not intended to influence readers’ decisions about investing or financial products. They should always seek their own professional advice that takes into account their own personal circumstances before making any financial decisions.

Expert tips on how to save, invest and make the most of your money delivered to your inbox every Sunday. Sign up for our Real Money newsletter.

Most Viewed in Money

Loading